(Bloomberg) — Upcoming readouts on the US labor market, including the monthly payrolls report, will give Federal Reserve policymakers insight into the need for further interest-rate reductions after an all-but-certain cut in a little more than two weeks.

Most Read from Bloomberg

With inflation slowing — although still running faster than the Fed’s goal — Chair Jerome Powell has telegraphed a September rate cut and said that officials “do not seek or welcome” further cooling in the labor market. Weeks earlier, government figures showed lower-than-expected July job growth and the highest unemployment rate in nearly three years.

This coming Friday, the August jobs report is expected to show payrolls in the world’s largest economy increased by about 165,000, based on the median estimate in a Bloomberg survey of economists.

While above the modest 114,000 gain in July, average payrolls growth over the most recent three months would ease to a little more than 150,000 — the smallest since the start of 2021. The jobless rate probably edged down in August, to 4.2% from 4.3%.

Two days before Friday’s report, the government will issue figures on July job vacancies. The number of open positions, a measure of labor demand, is seen easing to a three-month low of 8.1 million — just above a more than three-year low.

The number of vacancies per unemployed worker, a ratio the Fed watches closely, currently stands at 1.2, similar to pre-pandemic levels and a sign labor demand is roughly in line with supply. At its peak in 2022, the ratio was 2 to 1.

Also included in the job openings report are data on lay-offs and discharges. Any large increase could add to Fed officials’ concerns about a weakening labor market.

Other labor-related reports in the upcoming holiday-shortened week include weekly jobless claims and ADP Research Institute’s August snapshot of private payrolls. In addition, the Fed will issue its Beige Book of regional economic conditions, while the Institute for Supply Management reports purchasing managers indexes for manufacturing and services.

What Bloomberg Economics Says:

“Non-farm payrolls will likely improve from July’s disappointing reading – but the 818k downward revision in the BLS’s early estimate for the March 2024 benchmark period probably leaves Fed officials less willing to take the initial prints at face value.”

— Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins, economists. For full analysis, click here

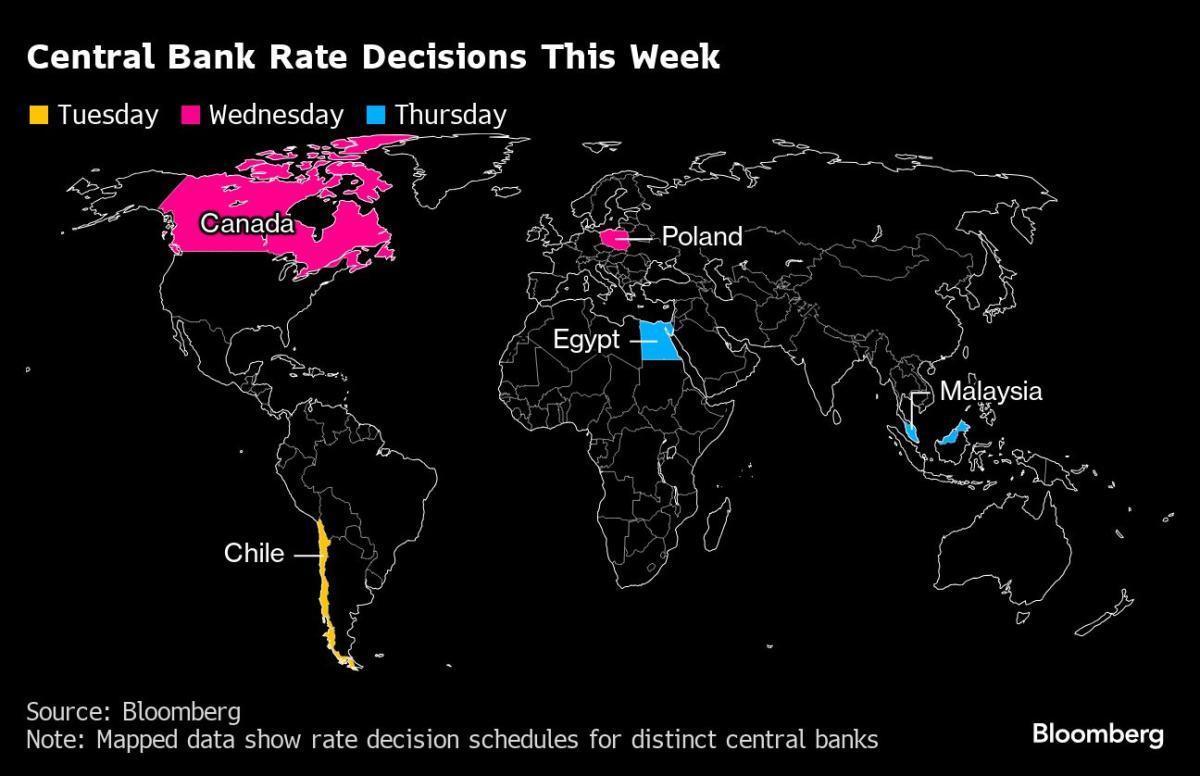

Elsewhere, the Bank of Canada is widely expected to deliver a third straight rate cut, as inflation that’s been within its target range all year allows officials to shift focus to weakness in the job market.

Purchasing manager indexes from around Asia, German industrial numbers and gross domestic product from Brazil are among other highlights.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

Asia

Asia begins the week with a wave of August manufacturing PMI data – including from Indonesia, South Korea, Malaysia, Thailand, Taiwan and the Philippines – following on from China’s official figures at the weekend.

China’s Caixin manufacturing PMI is also out on Monday, and is expected to show a return to expansion after a dip below 50 in July.

Japan on Monday gets a report on corporate performance in the second quarter. Capital investment may recover a tad after slipping in the three months through March, data that will feed into revised economic growth figures the following week.

In Australia, attention falls on current account figures that will also likely affect gross domestic product data. Those figures, due Wednesday, are expected to show that economic growth accelerated slightly from the prior quarter.

South Korea revises its second-quarter GDP the following day, and the region also gets a flurry of inflation updates. Trade data for August — published Sunday — showed that export growth returned to a double-digit clip, an outcome that bodes well for the economic outlook and reflects the resilience of global demand for technology products.

Vietnam’s consumer price gains may slow below 4% for the first time since March, while consumer-price data are also due from South Korea, Thailand, Taiwan, Indonesia and the Philippines. Trade statistics will be published in Australia, Vietnam and Pakistan.

Among central banks, Malaysia sets its overnight policy rate on Thursday and Reserve Bank of Australia Governor Michele Bullock delivers a speech the same day.

Europe, Middle East, Africa

Euro-zone policymakers have until the close of play on Wednesday to make comments before a blackout period kicks in ahead of their Sept. 12 decision.

With inflation now at a three-year low, a second rate cut for the newly-minted easing cycle looks increasingly likely. Central bank chiefs from Germany and France are among those scheduled for appearances.

The calendar for data is relatively light, with Germany likely to be a highlight. Factory orders on Wednesday and industrial production the following day will reveal the state of the country’s struggling manufacturers at the start of the third quarter.

Among regional reports on the agenda, a second reading of the euro-zone’s GDP measurement for the three months through June will be released.

The UK is likely to be similarly quiet, with final takes on August purchasing manager indexes for manufacturing and services scheduled for Monday and Wednesday respectively.

Consumer-price data in Switzerland may draw eyeballs in advance of the Swiss National Bank’s rate decision later this month. Inflation may stick at 1.3% for a third month, comfortably below the 2% ceiling for policymakers.

Turning east, in Poland — where data on Aug. 30 showed the fastest inflation so far this year — the central bank is widely expected to keep its key rate unchanged at 5.75% on Wednesday. Governor Adam Glapinski will speak at a news conference the following day.

Data from South Africa on Tuesday will likely show that the continent’s most industrialized economy skirted recession. Analysts expect the economy to have grown 0.5% in the second quarter after contracting 0.1% in the prior three months, helped by improved power supplies.

In Turkey, data is expected to show the inflation rate dropped by about 10 percentage points in August, to 52% from 62%. The central bank is hoping it declines to about 40% by year-end.

From Wednesday to Friday, African heads of and Chinese President Xi Jinping will gather in Beijing for the Forum on China–Africa Cooperation, where they’re expected to discuss new investment opportunities.

On Thursday, Egypt’s central bank is widely expected to hold its main rate at 27.5%. Some analysts, though, think it may opt to start the easing process now given the steady retreat in price pressures over the past year.

Latin America

Brazil on Tuesday will report second-quarter economic growth figures likely to reinforce that demand is shaking off the effects of tight monetary policy.

GDP is expected to have risen 0.9% quarter-on-quarter, more than during the first three months of the year, as a tight labor market and strong consumption propel activity.

The release will likely boost leftist President Luiz Inacio Lula da Silva, who’s raised public spending while pledging to improve living standards for ordinary citizens in Latin America’s largest economy. It could further pressure the central bank for interest rate increases as soon as in September.

The coming week will be crucial for economic data releases in Chile. On Tuesday, the nation’s central bank is likely to cut its key rate by a quarter-point, to 5.5%, after having paused the easing cycle at its prior meeting.

The next day, Chilean central bankers will publish their quarterly monetary policy report, with updated estimates on economic growth, inflation, and the future path for borrowing costs.

On Friday, the government will report August consumer price data, which is expected to show inflation accelerating further above the 3% target due to a series of electricity tariff hikes.

–With assistance from Matthew Malinowski, Piotr Skolimowski, Laura Dhillon Kane, Brian Fowler and Monique Vanek.

(Updates with South Korea trade in Asia section)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.