Nvidia (NASDAQ: NVDA) has been one of the hottest stocks on the market since the beginning of 2023, clocking stunning gains of 799% and outpacing the S&P 500 index’s 45% jump by a massive margin. This was due to the impressive growth in the company’s revenue and earnings due to the healthy demand for its artificial intelligence (AI) chips.

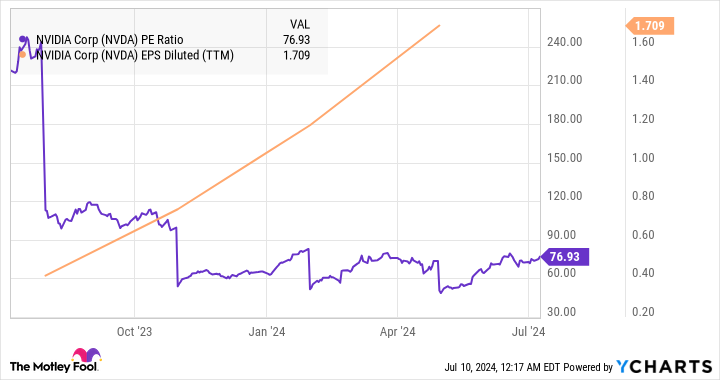

This phenomenal surge is why Nvidia is now trading at a rich valuation. Its price-to-earnings (P/E) ratio of 77 is well above the Nasdaq 100 index’s multiple of 32 (using the index as a proxy for tech stocks). This is why some Wall Street analysts are now concerned about the company’s ability to sustain its red-hot rally.

New Street Research recently downgraded Nvidia from buy to neutral, citing the stock’s valuation. Analyst Pierre Ferragu has a one-year price target of $135 on the stock, which points toward a very limited upside from current levels. Meanwhile, the stock’s median one-year price target of $130, as per 62 analysts covering the stock, also indicates that it’s unlikely to deliver more gains.

Does this mean it’s now time for investors to book their profits and sell Nvidia stock?

Can Nvidia continue to outperform the market’s expectations?

New Street Research believes that Nvidia stock could deliver more gains only if there’s a sizable increase in its outlook beyond 2025. It’s analysts aren’t convinced that this scenario is going to materialize just yet. The combination of Nvidia’s rich valuation and concerns about sustaining its terrific growth next year seems to have dented confidence in the company.

But a closer look at the potential growth of the AI chip market, which Nvidia dominates, and the company’s robust pricing power suggest it could indeed sustain healthy growth in 2025 and beyond. Market research firm TechNavio is forecasting the AI chip market will see an incredible annual growth rate of 68% through 2028, adding $390 billion in incremental revenue.

With an estimated 94% share of this market, Nvidia remains in a terrific position to capitalize on this opportunity. Of course, there’s competition from the likes of AMD and Intel in the AI chip market, but Nvidia is expected to remain the dominant player. For example, Citigroup expects Nvidia to control between 90% and 95% of the AI chip market in 2024 and 2025.

One reason that may be the case is because of the Nvidia’s ability to command a technology lead over rivals. Its next-generation Blackwell AI chips are already in full production, as management said on the latest earnings conference call. It also pointed out that the demand for Blackwell is “well ahead of supply, and we expect demand may exceed supply well into next year.”

It’s worth noting that Nvidia’s Blackwell chips are manufactured on a 4-nanometer (nm) node. For comparison, AMD’s flagship MI300X AI accelerator is reportedly manufactured on a 5nm and 6nm process. The smaller process node allows Nvidia to pack in more transistors, making its chips more powerful and energy efficient.

More specifically, the Blackwell chips pack 208 billion transistors, as compared to 153 billion transistors on the MI300X. This explains why the demand for Nvidia’s new processors exceeds supply. Moreover, even if Nvidia were to lose ground in the AI chip market in the future, its data center revenue is expected to multiply significantly, thanks to the massive addressable opportunity present in this space.

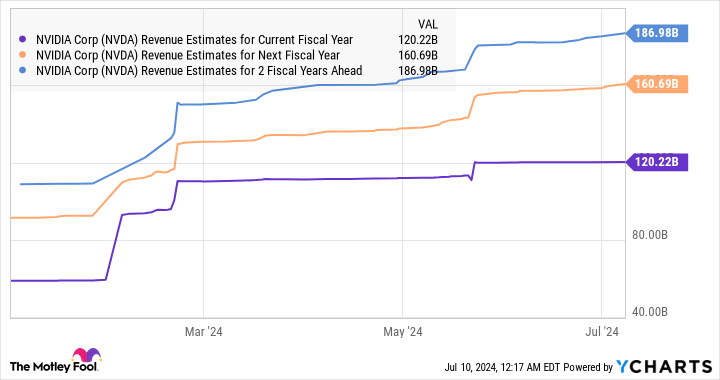

All this explains why Nvidia’s revenue estimates have been heading higher consistently of late.

Moreover, analysts are estimating Nvidia’s earnings to increase at an annual rate of 43% for the next five years. Based on its earnings of $1.19 per share in fiscal 2024, the company’s bottom line could jump to $7.11 after five years. Multiply that with the Nasdaq 100’s forward earnings multiple of 29.5 and Nvidia’s stock price could increase to $210, implying a 60% upside from current levels.

It may not be a good idea to sell shares of Nvidia right now, and a closer look at the company’s valuation indicates it isn’t really expensive when considering the growth that the stock is expected to deliver.

The chipmaker’s valuation is justified

While it’s true that Nvidia stock is expensive right now when compared to the broader index, it would be wrong to take a look at its valuation in isolation. The company delivered a 262% year-over-year increase in revenue in fiscal Q1 to a record $26 billion, along with a 461% increase in adjusted earnings. For comparison, the S&P 500 index’s earnings grew an estimated 7.1% in the first quarter of the calendar year.

As it turns out, Nvidia’s rapid earnings growth is why its P/E has dropped in the past year, signifying that it’s been able to justify the premium valuation.

The company’s forward P/E ratio of 48 isn’t very expensive considering that the U.S. technology sector has a similar earnings multiple. So selling Nvidia stock based on its valuation doesn’t look like a good idea. The terrific growth that it’s been delivering and its ability to sustain it could result in more upside in the long run.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,968!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,001!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $352,022!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of July 8, 2024

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

Is It Finally Time to Sell Nvidia Stock? was originally published by The Motley Fool